Despite decreasing sales, businesses' equity strength remains good in this sector, but larger groups and producing companies are usually better capitalised than wholesalers or retailers.

- Decreasing sales in 2015

- More insolvencies expected in the long term

- Fraud cases remain an issue

According to the German Food Association BVE, nominal turnover decreased 1.7% in 2014, to EUR 172.2 billion. This was followed by another 4.4% decrease in H1 of 2015, reaching EUR 81.9 billion. While domestic sales decreased 6.5%, to EUR 55.8 billion, export sales recorded modest growth of 0.5%, increasing to EUR 26.1 million. Real turnover (domestic and export) declined 2.1%.

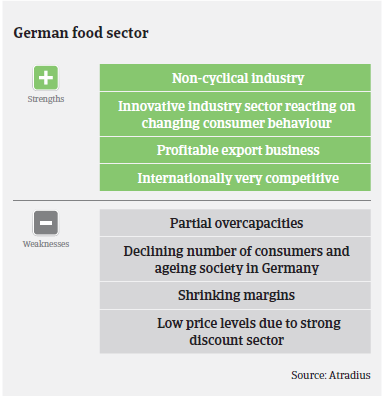

Despite decreasing sales, businesses’ equity strength remains good in this sector, but larger groups and producing companies are usually better capitalised than wholesalers or retailers. In terms of solvency and liquidity, larger companies are normally better financed than smaller ones. The overwhelming market power of large retailers and discounters and the tough competition and price wars in the food retail sector indicate that food producers, processors and suppliers have found it difficult to pass on costs. As a result, their profit margins have decreased in recent years and are continuing to decline. In the last couple of years food discounters in particular have changed their supply practice, reducing the number of suppliers and focusing on a lower number of larger suppliers.

Nevertheless, despite the problems in the industry, many companies in all food subsectors are doing well. The food sector is non-cyclical, and thus less volatile than other industries. Moreover, the sector’s export share has almost doubled since the mid-1990s, providing business opportunities abroad. However, while businesses with strong export orientation have tried to increase sales to other export markets after the Russian food import ban, success has been limited so far.

Meat/meat products is by far the largest subsector, controlled mainly by a few market-leading meat processors who, over recent years, have created fully vertically integrated groups. The rising demand for meat worldwide has provided business opportunities for the German meat industry, with a boost to the profit margins of those with the largest export share. However, overcapacity in the German meat and meat processing sector means that suppliers of non-essential products and those that do not export are in danger of sooner or later being squeezed out of the market.

After positive developments in 2013 and early 2014, thanks to high milk prices and increasing volumes, milk farmers have suffered from substantially decreasing milk prices in 2015. However, the sector benefits from specific EU subsidies.

Due to slightly decreasing market prices, which result from increased available market volumes (also due to the Russian food import ban), turnover is not increasing as much as sales volumes. As a result, profit margins are decreasing.

Despite lower raw material costs for cereals and sugar, sales prices in the German beverage industry (beer, mineral water, soft drinks etc.) remain under pressure because of lower consumption, increasing consumer price sensitivity, overcapacity and discounting. The German beer sector is facing continuing market concentration and consolidation and changing consumer behaviour. The number of breweries still appears too high and many are too small to be competitive. In an attempt to reverse the industry-wide decline in sales of beer, many German breweries have begun to offer innovative beer-mix drinks with lower alcohol level or to produce craft beer, which are and probably will remain niche products without significant market shares. Profit margins continue to shrink in this segment.

Food producers and wholesalers pay, on average, within 30 days while payment terms of food retailers often vary between 45 and even 90 or more days. We have not seen any increase in the number of notified non-payments in the last couple of months and do not expect this in the near future.

With food processing companies and retailers demanding longer payment terms from their immediate suppliers to improve their working capital, a wave of longer payment terms is being created along the whole supply chain. Still, the already low profit margins are further decreasing. Due to the still strong economic environment in Germany, food insolvencies have not increased recently. However, in the medium term the number of defaults could rise, especially for smaller businesses and those with poor financial strength.

As the food sector´s performance is still robust, our underwriting stance remains generally relaxed, although we can usually provide cover on buyers who have operated for less than a year only if they are affiliated to well-established companies or groups. If there are signs that a buyer’s finances are deteriorating, we will increase our monitoring, with quarterly reviews and requests for recent reports of payment experience.

The food sector has seen considerable fraud cases, which are still rising and getting increasingly tricky and professional. Therefore we pay close attention to the number of credit limits that are applied for within a short period, especially where the buyers are recently established and where management and/or shareholders have recently changed or the buyer’s business sector does not match with the goods ordered (e.g. a steel company ordering food items).

Lisämateriaalia

937KB PDF